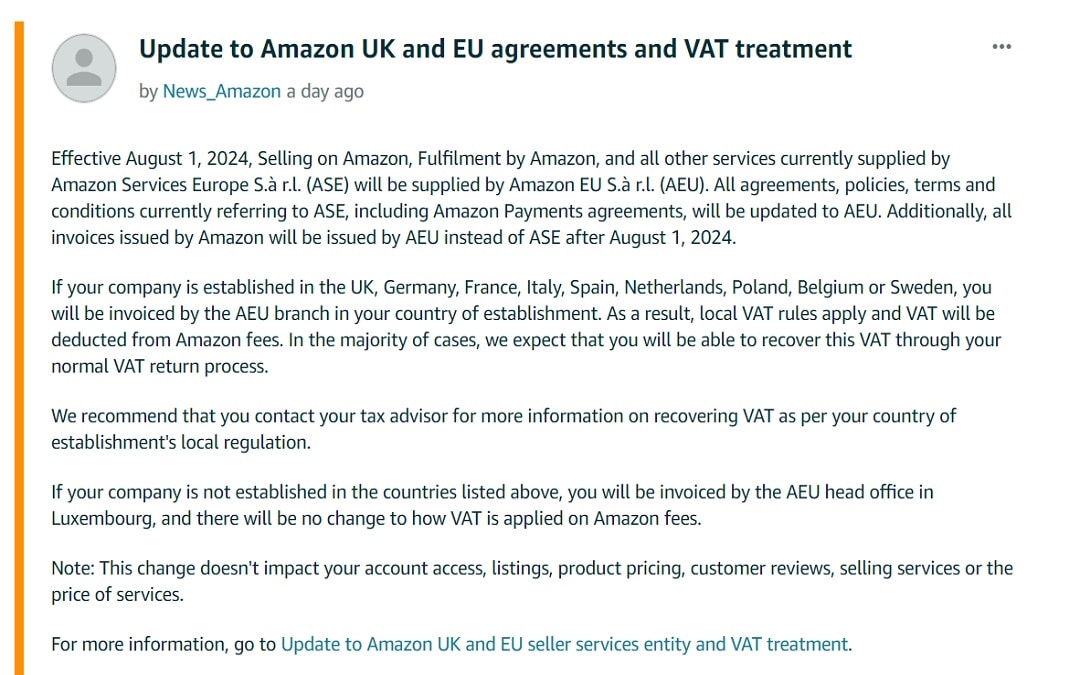

Amazon sellers in the UK, Germany, France, Italy, Spain, the Netherlands, Poland, Belgium, and Sweden have all recently received a notification from Amazon that the Vat treatment of fees will change from 1 August 2024. The notice refers to “Selling on Amazon, Fulfilment by Amazon, and all other services currently supplied by Amazon Services Sarl (ASE)…” which essentially means selling and FBA fees. It does not have any impact on the way that advertising fees are currently invoiced, as these are not currently billed by ASE.

Currently, ASE bills from Luxembourg and the fees are subject to the Reverse Charge Mechanism. This means that no VAT is added to Amazon’s charges, but the seller accounts for the VAT that would have been charged in their own territory, on their domestic VAT return, as sales VAT, but also claims it back on the same return as input VAT (under the reverse charge mechanism).

From 1 August, these fees will be billed from Amazon branches established within each territory. UK companies will therefore be billed from the UK, German companies from Germany etc. This means that domestic VAT will be charged on these fees where applicable.

What is the Cashflow Impact of These Changes?

Whilst there is no additional costs to most businesses, there will be a negative cash flow impact. This is because 20% (if UK VAT applies) will be added to Amazon’s fees and sellers will have to claim this back on their VAT return, thus causing a cash flow disadvantage.

How Much Impact Will These Have on My Business’ Cashflow?

Let’s say a business has sales of £200,000 per VAT quarter. If selling and VAT fees are 35%, which is fairly typical in round terms, then fees will be £70,000 per quarter and the VAT now being charged will be £14,000. The £14,000 of VAT will be paid to Amazon throughout the quarter, and the reduction in that business’s VAT liability will not be felt until the quarterly VAT is paid almost 6 weeks later. During that 6 week delay another 6 weeks of VAT will have been paid on fees to be reclaimed the following quarter, likely to be another £6,000. The peak of the cash flow dis-advantage could therefore be as much as £20,000. As a rough estimate, we would expect the peak cash flow impact for a 100% Amazon business to be as much as 10% of revenue.

How Might the Changes Impact Profitability?

Small business using the flat rate scheme will be disadvantaged. When using the flat rate scheme no input VAT is reclaimed (except in limited circumstances) as the percentage applied to revenue to determine the value of VAT payable makes an allowance for input VAT. Reverse Charge expenses currently have no impact on the amount of VAT payable on each return. If VAT is now being charged on fees then the VAT liability on each return remains the same, but the business will have paid more VAT on its costs and this could make the flat rate scheme less attractive. Even if the scheme remains the best option for a business, profits will be impacted by the amount of additional VAT being paid from 1 August.

Start up will also be adversely impacted. In most instances, a start up will not register for VAT until required to do so (£90,000 revenue). By default, Amazon charges these businesses VAT on their fees, but if evidence is provided to Amazon that a seller is in business then Amazon fees are also subject to the Reverse Charge Mechanism, so no VAT is charged. Under the new arrangements, VAT will always be charged on Amazon fees, which will impact a start up profits.

How Will the Changes Impact on Vat Registration Requirements for UK Sellers?

On the flip side, a start up that has proven to Amazon that they are in business and is not being charged VAT will not reach the VAT registration threshold quite so quickly. This is because the reverse-charge transactions count towards a business’s turnover when measuring income against the VAT registration threshold. Under the new arrangements, the Amazon fees will have no impact on a business’s turnover for VAT registration purposes.

What Can I Do to Mitigate the Impact?

Many Amazon sellers will import their product from overseas and will be paying import VAT when the goods enter the UK. There is a process by which this VAT can be postponed. If a business is not doing this already, they should start to do so now.

If the cash flow impact is a concern, then there are various options for working capital facilities or even funding specifically for VAT bills spread over 3 months. If you have sales to the EU you will have sales on which no UK VAT is due, but will be incurring Amazon fees on those sales on which UK VAT will be charged. If those fees are significant, it is possible that your VAT returns could result in repayments going forwards. In these circumstances, you could consider asking HMRC if you could submit monthly VAT returns in order to receive your refunds more quickly and regularly.

How Can We Help?

At Elver E-Commerce Accountants we specialise in assisting e-commerce businesses with the unique tax and accounting challenges that e-commerce businesses face, whether that is navigating the complexities of accounting for e-commerce sales, VAT, both domestically and internationally, to cash flow forecasting, management accounts, sourcing and assisting with loan applications and advisory services. If you would like to discuss how we can help, please call 01942 725419 or use the contact form to book a meeting.